Medicare.gov - Tutorial - Additional Medicare Plan Details

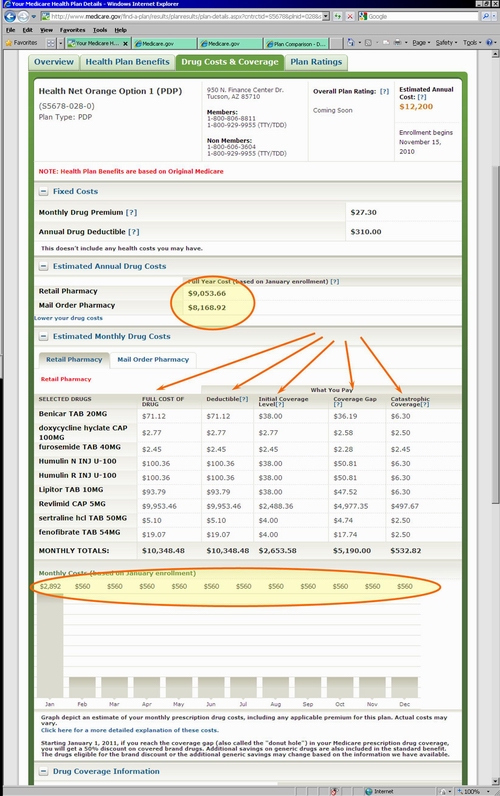

When we take a closer look, for example at the example plan in the screen shot, we see a summary of what we learned previously from the Medicare Plan Finder. Again we see the Medicare Part D plan contact information and then the projected annual prescription drug plan cost as compared to the cost if Mail Order is used.

If the option is chosen to "Add More Drugs", you will be returned to the drug search form. When you have completed adding more drugs, you will again be asked about your pharmacy preferences and then arrive back at the Medicare plan overview or summary page.

Now back to learning more about the plans. Medicare suggests that you choose a Medicare Part D plan based on the 3 "C’s": Cost, Coverage, and Convenience. We would add to this a fourth "C" that is important to many people: "Company". Everyone should ensure that their medications are covered (or at least their more expensive medications). Some people are looking at only cost — which Medicare plan will cost the least across the whole year. Some people will pay more annually for a Medicare Part D plan just to have no initial deductible ($0 deductible or first dollar coverage). Some people will pay more for their medications just to have a lower monthly premium. Some people only want the convenience of knowing that their local neighborhood pharmacy will accept their Medicare Part D plan so that they will not need to visit a chain pharmacy. Some people choose a Medicare Part D plan based on the underlying company — they select ABC Insurance Company, because they have always worked well with ABC Insurance Company.

Bottom Line: Everyone has a way to select a Medicare Part D prescription drug plan that is right for them. We usually suggest that you choose the Medicare Part D plan or Medicare Advantage plan that provides the most affordable health and prescription coverage and best service throughout the whole year.

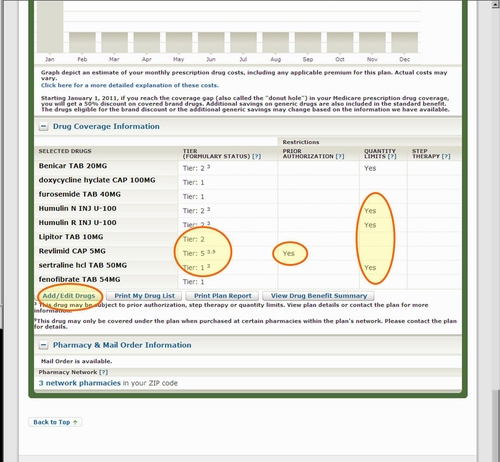

In the graphic above, you can see the medications are sorted by formulary or drug list tiers. Usually the higher tiers are reserved for more expensive or exotic medications, and this is true with this plan's Tier 5. Several of the medications also have certain formulary restrictions including Prior Authorization (where you need to receive written approval from the Medicare plan before filling a prescription, usually your prescribing doctor will help you with the Prior Authorization form) and Quantity Limits (you are allowed coverage for a certain amount of your prescription each month or other time limit). No medication in this example falls into having Step Therapy (you are asked to try another, less expensive medication before being allowed to use this prescription.).

- No enrollment fee and no limits on usage

- Everyone in your household can use the same card, including your pets

- Sign-up for our Medicare Part D Newsletter.

- PDP-Facts: 2024 Medicare Part D plan Facts & Figures

- 2024 PDP-Finder: Medicare Part D (Drug Only) Plan Finder

- PDP-Compare: 2023/2024 Medicare Part D plan changes

- 2024 MA-Finder: Medicare Advantage Plan Finder

- MA plan changes 2023 to 2024

- Drug Finder: 2024 Medicare Part D drug search

- Formulary Browser: View any 2024 Medicare plan's drug list

- 2024 Browse Drugs By Letter

- Guide to 2023/2024 Mailings from CMS, Social Security and Plans

- Out-of-Pocket Cost Calculator

- Q1Medicare FAQs: Most Read and Newest Questions & Answers

- Q1Medicare News: Latest Articles

- 2025 Medicare Part D Reminder Service